by Edward Hugh

Marty Feldstein

has an article in the Financial Times today under the header "Immigration is no way to fund an ageing population" (or

here). This is a strange coincidence since earlier this week I was busy posting on

Italian Economy Watch about

the boost given to economic growth in Italy in recent years by the growing numbers of immigrants who have been arriving there.

Now since I am arguing that immigration is in fact a significant policy tool which can be leveraged to address the problems raised by population ageing, a clear clash of opinions would seem to exist. So who is right here?

Actually the article is a summary of

a recent paper which Marty Feldstein has published at the NBER:

The Effects of the Ageing European Population on Economic Growth and Budgets: Implications for Immigration and Other Policies Unfortunately the paper is only downloadable for those who have access to a university server, but I would encourage those who can to read the full paper, since I think the differences of opinion here go to the heart of many of the important issues in the 'ageing' debate, and it is important to have both sides of the story. That being said, I think most of what follows is comprehensible even if you can't read the paper (especially if you use the FT article as a back-up).

Firstly here's the paper abstract:

The ageing of the population presents a major fiscal challenge for the countries of Europe. The combination of increased longevity and a reduced birth rate will directly reduce the growth rates of the European economies by slowing the growth of the capital stock and by weakening the productivity of the labor force. This slower growth of GDP means a smaller tax base and less tax revenue. In addition, the current tax-financed systems of social pensions and health care will require substantial increases in the already high tax rates. The analysis in this paper shows that the common prescription of increased immigration would do little to reduce the future fiscal burden. The increased revenue from a large rise in immigration would finance only a small part of the coming rise in the cost of pension and health benefits. The only alternative to significantly higher tax rates or substantially lower retirement income is to shift from a pure tax-financed system to a mixed system that supplements the tax financed benefits with benefits based on increased saving financial investment.Now most of the points here are hardly new, but Feldstein's argument does have the virtue of being put simply, and in a non-technical fashion (which is why it is a pity that the whole paper is not more generally available to non-economists). Feldstein wants to argue that:

There may be many reasons to favour increased immigration....But it would be wrong to advocate increased immigration as necessary to deal with the fiscal consequences of an ageing population, or as a means to avoid large future tax increases or benefit reductions.As we will see later this argument really comes in two parts:

i) that immigration is not necessary to deal with the fiscal consequences of ageing populations

ii) that immigration constitutes a way of handling ageing which enables you to do so without large tax increases or benefit reductions

On the first argument I want to suggest that Feldstein is simply wrong. Immigration is necessary to facilitate the handling of the fiscal consequences of ageing populations (where and for as long as it remains a possible policy option) in easing the process of transition away from Paygo systems.

On the second he is much nearer the point, as I see it immigration is simply one part of a policy tool kit, a kit which also should include pro-natalist policies, increased retirement age, tax increases and benefit reductions. Some combination of all of these is necessary, the 'in the ballpark' debate centres around precisely what mix is feasible and desirable.

Actually I would argue that the mix you can apply depends in part on the point in the demographic transition from which you start. Obviously if you are a country with a still comparatively young median age (say the UK or France at around 38) you have a far broader range of options in front of you than have Italy, Germany and Japan (whose median age has already risen to 43). Since the demographic transition is all about rising median ages, the importance of this point, and of acting sooner rather than later, should not be lost on anyone.

The core of Feldstein's argument is really the following:

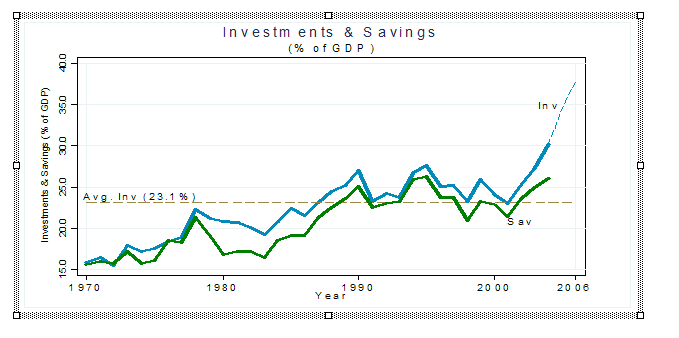

Consider first the effect of slower population growth on the national saving rate. At any point in time, there are some households that are savers (i.e., consuming less than their entire after-tax income) and other households that are dissavers (borrowing or using up some of their previous saving). The savers are predominantly middle aged employees who are preparing for retirement. The dissavers are typically in their retirement years. In a growing economy there are relatively more middle-aged savers than there are older dissavers. That, together with rising per capita income, is what causes the saving of the savers to be greater than the dissaving of the dissavers. That difference between the saving and the dissaving creates a positive saving rate for the economy as a whole. The faster the population growth rate, the higher will the nation's saving rate tend to be. That explains why the aging of the population and the slower rate of population growth cause a decline in the share of national income that is saved.Now this argument is both right and wrong in my opinion. Basically what he is saying is true IN THE VERY LONG RUN. But it entirely misses the point that we on Demography Matter have been trying to focus attention on, which is THE TRANSITION DYNAMICS of the ongoing demographic changes.

Especially I would draw attention to this phrase:

That explains why the aging of the population and the slower rate of population growth cause a decline in the share of national income that is saved.If we are to address this issue adequately then we need to start from the current reality, and from what we actually know of the economic dynamics of population ageing, and what better place to start than with those three famous prominent elderly societies that I tend to go on so much about - Germany, Japan and Italy. These three are important since they are the ones who have gone furthest with the transition. Now if we look at them as a group the first thing which we should note is that they are hardly to be singled out for an absence of savings. At the same time we could note that all those equally famous 'anglo' consumer debt societies - the ones where saving constitutes a pretty low share of national income - seem to share the characteristic that they are - in population median age terms - significantly younger. So what I think is that we have a calibration problem here in the application of the life cycle savings and borrowing model to populations (read

Modigliani for the life cycle theory here), and strangely very few people seem to date to have woken up to this. Massive dis-saving may of course come one day (although this isn't as clear as it seems to Feldstein, since, and possibly for reasons like presence of bequest motives, people do not seem to dis-save that dramatically as they age). That ultimate theoretical possibility should not detain us too much at this point, however, since it should really be what happens before we get to the dis-saving median ages that holds most of our attention at the present time, since if some part of the whole demographic transition process is

path dependent, then what happens earlier should be considered to be important as it may well influence what happens later.

Also the following assertion from Feldstein - in a globalised world - doesn't necessarily hold:

This lower rate of saving will in turn lead to a lower rate of investment in business plant and equipment.since as we all know the saving which is needed may simply take place elsewhere (as we can see from the case of the United States at the present time). Now in fairness to Marty he does immediately qualify his argument when he comes to look at Spain (which is his test case, presumably since Spain has been the recent recipient of quite a lot of immigrants and it is really this component he wants to look at):

Although in principle Spain could in the future supplement its lower saving rate by importing capital from other countries, this is not likely to happen in practice for two different reasons. First, the other industrial countries are also experiencing slower population growth and that will cause their saving rates to decline. So they too would want to import capital and would not be in a position to shift capital to Spain. Moreover, experience shows that, oversustained periods of time, industrial countries invest what they save at home. So even countries with higher saving rates will tend to keep the extra saving at home.

What he is actually missing here is that the demographic transition is in fact evolving in a very uneven fashion, and this can be seen from

a quick glance at the respective median ages of the OECD countries. There will be,

as Claus Vistesen is following, international capital flows (and

here), and these will form part of the overall transition dynamics. Indeed it is here that we should expect the path specific components to be important in determining winners and losers.

That is why (for example)

this post from Claus is also interesting about the topic of growth and immigration, since it looks at empirical work from the Bank of England on the impact of immigration in the UK, and it is precisely this point about the impact of immigration on transition dynamics which I think more or less invalidates the thrust of the argument that Feldstein wants to make. Obviously if, say, Spain manages to leverage immigration to delay the arrival of a median age of 43 by 20 years then Spain will have bought time, and time in this case is very much knowledge, since we will have learnt a lot more about all of this twenty years from now.

So what I want to argue is that while immigration certainly cannot solve the long term demographic transition steady-state problem, since high median ages eventually come to everyone, it is also important to bear in mind that here, as ever in economics, timing does matter (again, this appreciation is the real legacy of Keynes). As we all know only to well, in the long run we are all dead, but even if we imagine that at this point - in an extremely theoretical sense - as a species we are going to become extinct at the rate we are going given the steady extension of below-replacement fertility rates, this doesn't really mean that this has become an immediate issue, and sometimes it is worth focusing on immediate issues and leaving tomorrows problems for tomorrow's generations (always provided we do this responsibly).

At the same time I would like to say that Marty Feldstein is, of course, a very able economist (and indeed he was one of the first in the 1980s to sound the wake-up call among economists about the whole ageing issue), so please don't miss the fact that he does make many very valid points. Such as this one for example:

"An aging work force also lowers productivity growth directly. We know from experience that each generation of employees earns more than the previous generation. One reason for this is the improved level of education and of skills that the new generation brings to work. We are all aware of the greater facility that younger workers generally have in using computers and the internet. Younger workers also generally learn new skills more readily. So an aging workforce means lower increases in productivity from this source as well."This is noteworthy since there would many who would try to avoid drawing this conclusion, but as

I attempt to argue in this post, there are sound theoretical reasons for thinking that Feldstein is right here.

On the other hand Feldstein seems to completely miss another important part of the overall picture, which is the fact that we are currently seeing a dual process of weakened internal consumption in the elderly trio (Japan, Germany and Italy) and a chain of trade and international-capital-flow imbalances (that are in fact at the very centre of contemporary macroeconomic debate) which can very plausibly be argued to have something to do with the differential demographics of the various countries involved.

For one summary of how these two elements (demography and imbalances) may be inter-related

see this paper by Ralph Bryant, which *is* downloadable (although also note that it is in pdf format):

"

Asymmetric Demography and Macroeconomic Interactions Across National Borders"

This post

on ageing and consumption on Italian Economy Watch and

this one on the Median Ages issue also provide some further background arguments, as do

this whole slew of posts on Japan from Claus Vistesen.

Now I have one last niggle before I finally shut up. I sometimes wish economists were forced to do a short course in philosophy, logic and reasoning. because at times I feel they need to learn the meaning of logical quantifiers like "some" and "all", quantifiers which seem to be so vital to a healthy reasoning process. Take this as one bad example of how not to reason:

Although there is general discomfort with some of the social consequences of increased immigration, many people have concluded that increased immigration is the "only way" to avoid a major increase in tax rates or a major cut in benefits.Now what I would ask Marty directly is just who these people are who have reached the conclusion that "the only way" to avoid a major increase in tax rates or a major cut in benefits is immigration (we wouldn't want to be demolishing a straw man, now would we?). In fact I doubt that there is anyone who has seriously thought about the problem who thinks it is possible to avoid some measure of both spending cuts and increased taxation. Indeed immigration is not part of any "only way" strategy anywhere to my knowledge. Certainly the EU's Lisbon Agenda doesn't say this, and indeed far from it. Those of us who are on the

Demography Matters Blog are perhaps among the people who have taken the 'positive impact of immigration' argument farthest, but to my knowledge we are only saying that immigration can *help*, and for the reasons outlined above (many of which Feldstein fails to appreciate the importance of).

In fact the main argument he addresses is this one:

The presumed advantage of increased immigration as a policy response to the aging population is that it would help to finance the benefits of the aged.As I am saying, I don't think this is the *only* presumed advantage. Again it is obvious that immigration can help fund taxes in the short term, but the force of the argument about such immigration is that this short term benefit helps buy time and offers us all a pathway to try and equilibrate the global imbalances which, at the end of the day, are the heart of the problem.

Actually I would only too readily agree with this point:

Stated differently, the increased revenue from a large rise in immigration would finance only a small part of the coming rise in the cost of pension and health benefits.And again Marty is not entirely off-target when he talks about the ways in which the Lisbon agenda is being interpreted at nation state level, and in particular in Italy, and Germany where a very heavy reliance is being placed on raising taxes rather than cutting spending, and as we may well be about to see this can prove to be very problematic, so I don't disagree with him at all here. But I'm not entirely sure that it is the Lisbon agenda itself that is responsible for this, as opposed to the ridiculous way in which the EU Growth and Stability Pact has been trivialized and effectively ignored. Of course this deaf ear will ultimately come with a price.

There is one last issue raised in the paper which I would like to touch on in this post, and it is the following one:

Shifting from the current pure pay-as-you-go tax financed systems of pensions and health care to financing based on a combination of taxes and financial investments could reduce the burden on future generations of employees and taxpayers without lowering the standard of living of future retirees.In principle this idea is sound and has merit, but methinks it is not as straightforward as it seems. Indeed I could at this point throw the ball back to Feldstein and say that if this is the *only* policy instrument deployed, then it simply won't solve the problem. There are two main issues presented here, and I would like to try and explore both of them in more depth during the course of 2007:

1/. The saving and investment consequences of a change in the way pensions are funded may not be quite the ones which Feldstein anticipates, since obviously (as he to some extent recognises) there will be consequences for the savings behaviour of the younger age groups. The changes will effectively mean that these groups have both to pay taxes to finance the outstanding liabilities to those who are already old and save for their own private pension plans. There is no doubt that this has to happen, but there are issues about how rapidly this can take place without crashing consumption. This is where the immigration argument does become important. Since Feldstein does not address the consumption issues he just doesn't see this part.

In the US there is no doubt that any such savings shift would be beneficial, but then we get to the 'uncoupling' issues

which so preoccupy Claus Vistesen. How does the rest of the world - and in particular those countries who need to run surpluses, handle this situation?

Also, even though I have been drawing attention to the relatively high saving which is taking place in Japan etc, we really have no measure of whether these countries are doing *enough* saving in relation to the challenges they face (private saving has been in secular decline in Japan in recent years), and this is just one more topic which economists in general need to start getting to grips with. But if such countries need to start to save even more, what does this imply for the level of exports they will have to depend on, and where exactly will all these exports go?

2/. Feldstein (and indeed most other commentators) assume that private pensions can offer a good rate of return:

But because the rate of return on an investment based account is much greater than the implicit return in a pure tax-financed system, the amount of saving that is needed is much less than the amount of additional taxes that would otherwise be required.Again formally speaking this is surely true, but just what rate of return can be offered? No-one really knows. In fact the issue of just the level of the rate of return on private pension funds is much more a problem than that old bogey of 'stock market meltdown', but the problem isn't being thought about sufficiently. Actually the whole central bank debate about global liquidity has something to do with this (and I can't help asking myself whether in the background the central bankers are not in fact bright enough to be actually thinking about this one), and clearly the savings glut is also to do with the investment dearth, but how do you maintain a good rate of return when the ratio of savings to investment rises sharply globally. The whole debate about increasing risk appetite and emerging markets is surely to do with this.

So with increasing dependence on private schemes this problem would only grow, as the level of funds looking for a viable rate of return will only increase, and struggle as they might the central bankers will find it hard to push interest rates up significantly with so much liquidity floating around.

This is why I feel putting the focus on global imbalances is so important in this context, and it is also why I think it important to find policy solutions which take the imbalances as their starting point, since they are surely at the heart of the problem.

One last small gripe: why do people keep putting the focus on this as a purely European issue? (Note the title of Feldstein's paper). Declining fertility and increasing life expectancy is a global phenomenon, and if we are ever to find a way of adequately handling population ageing then I think we need to see this as a global, and not a national level problem. The real issue posed by the pyramid inversion which is associated with the ongoing demographic transition is actually how to shift from a paygo to a post-paygo environment with the least possible collective damage. That not everyone in the United States has quite the limited perspective on this that Marty Feldstein seems to have

can be seen from this recent speech from Ben Bernanke.